You’ve built some equity in your home — now you’re wondering if it can work for you. Enter the home equity loan, one of the more traditional ways to tap into the value of your house without selling it.

But here’s the catch: home equity loans aren’t free money. They come with risks, paperwork, and long-term commitments. This guide will help you understand exactly what’s on the table, who home equity loans make sense for, and what the options really look like in today’s market.

First, What Is Home Equity?

Let’s break it down:

Home Equity = Your home’s market value – What you still owe on your mortgage.

Example:

Your home is worth $400,000 and you owe $250,000 on your mortgage.

You have $150,000 in equity.

Lenders usually let you borrow up to 75%–85% of that equity, depending on your credit score, income, and the type of loan.

What Is a Home Equity Loan?

A home equity loan is a second mortgage. You get a lump sum of cash upfront and pay it back in fixed monthly payments, typically over 5 to 30 years.

- It’s secured by your home — miss payments and you could lose it.

- Interest rates are typically lower than personal loans or credit cards, but higher than your primary mortgage.

Think of it as a structured, lower-interest way to borrow a chunk of money — but one that puts your house on the line.

Common Reasons People Take Out Home Equity Loans

A home equity loan can make sense in many real-world scenarios:

- Major home renovations (new roof, room addition, HVAC replacement)

- Debt consolidation (paying off high-interest credit cards)

- Medical expenses not covered by insurance

- College tuition or education costs

- Emergency expenses (but only if you’ve run out of better options)

- Business funding (self-employed folks often leverage home equity)

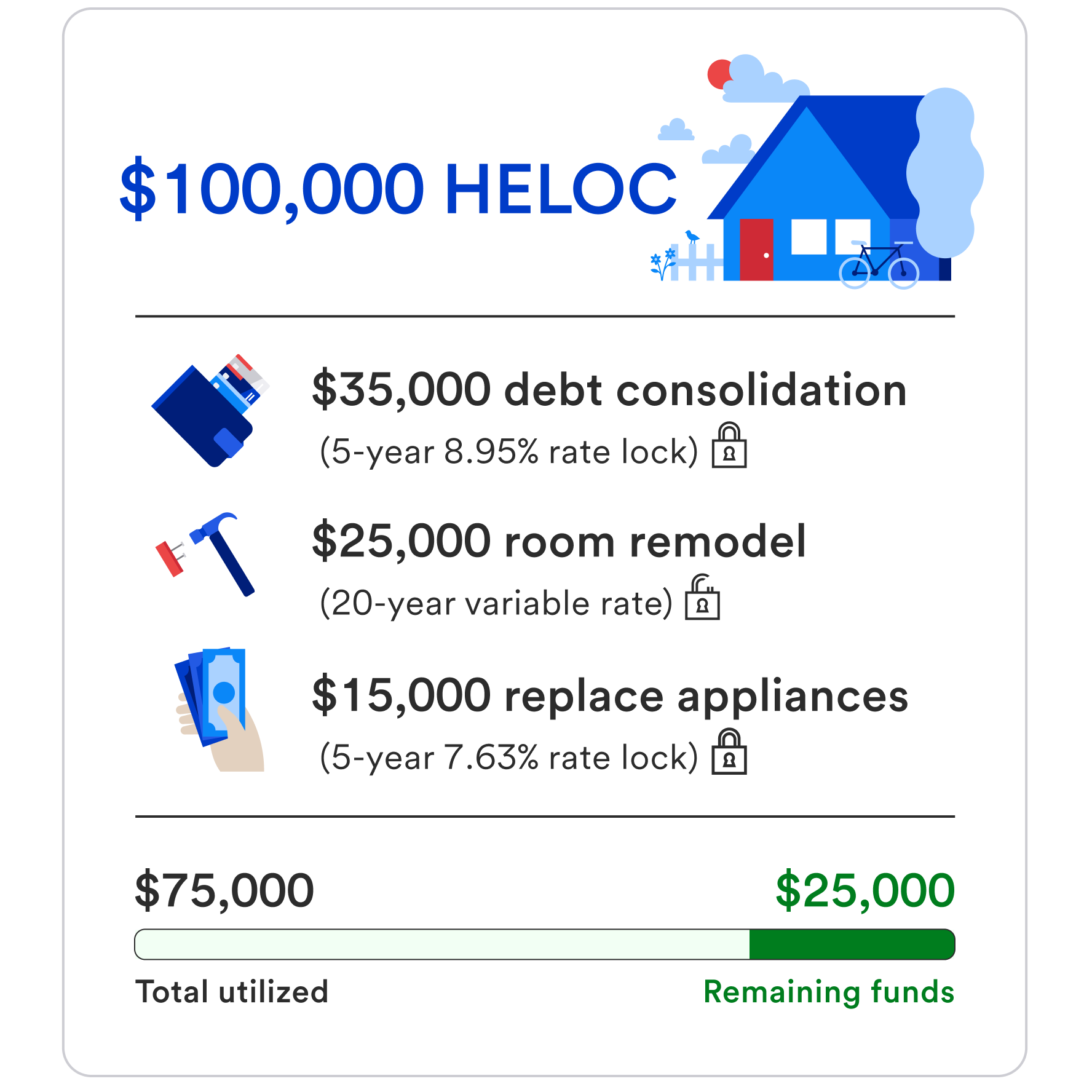

Home Equity Loan vs. HELOC: What’s the Difference?

People often confuse these two — here’s how they differ:

| Feature | Home Equity Loan | HELOC (Home Equity Line of Credit) |

|---|---|---|

| Payout | Lump sum | Borrow as needed (like a credit card) |

| Interest Rate | Fixed | Variable (usually) |

| Repayment | Starts immediately | Draw period + repayment period |

| Monthly Payment | Predictable | Varies based on balance and rate |

| Best For | Large, one-time expenses | Ongoing or uncertain expenses |

If you know exactly how much you need and want fixed payments, go for a loan. If you need flexibility, look into a HELOC.

Pros and Cons of Home Equity Loans

Pros:

- Lower interest rates than personal loans or credit cards

- Predictable monthly payments

- Interest may be tax-deductible if used for home improvement

- Can significantly reduce interest if consolidating debt

Cons:

- Your house is collateral

- Closing costs can be 2%–5% of the loan

- Less flexibility than a HELOC

- May increase your overall monthly debt load

Home Equity Loan Providers and What They Offer

Here’s a breakdown of major lenders currently offering home equity loans in the U.S.:

| Lender | APR Range | Loan Amount | Terms | Notes |

|---|---|---|---|---|

| U.S. Bank | ~8.20% – 11.80% | $15,000 – $750,000 | 5 – 30 years | No closing costs in some states, must have good credit |

| Bank of America | ~7.99% – 11.49% | $25,000 – $500,000 | 10 – 30 years | Fixed rates, discounts for existing customers |

| PNC Bank | Varies by state | $10,000 – $500,000 | 5 – 30 years | Option to apply online or in person |

| Wells Fargo | (HELOC only) | — | — | Previously paused home equity loans; check availability |

| Figure (online lender) | ~6.50% – 13.50% | $20,000 – $400,000 | 5 – 30 years | Fast funding, online-only process |

| Discover | ~6.24% – 11.99% | $35,000 – $300,000 | 10 – 30 years | No origination fees, direct-to-consumer approach |

Costs and Fees to Watch Out For

Before you celebrate your approval, here’s the fine print to watch for:

- Origination or application fees

- Appraisal fees (often required for home value verification)

- Title search and closing costs

- Prepayment penalties (less common now, but still worth asking about)

Some lenders waive closing costs, but that may be conditional on keeping the loan open for a set period (often 36 months). Close it early, and you might have to repay those waived fees.

How to Know If a Home Equity Loan Is Right for You

Ask yourself:

“Am I borrowing to build value — or just to stay afloat?”

A home equity loan can make sense if:

- You have significant equity in your home

- You have a strong credit profile and can qualify for a good rate

- You’re using the funds for a high-ROI purpose (like necessary home improvements or high-interest debt consolidation)

- You’ve run the numbers and can handle the monthly payments comfortably

It might not be the best choice if:

- Your income is unstable or uncertain

- You’re already stretched thin with other debts

- You’re tempted to borrow for wants, not needs

A home equity loan can be a smart way to tap into the value you’ve built — if you use it strategically. Like any loan, it’s not just about qualifying. It’s about whether the math (and the purpose) truly works in your favor.

Remember: You’re putting your house on the line. If that risk makes you nervous, you’re not alone. Just be sure the upside is worth it.